Financial highlights

Last trade 55.12€

Variation +2.61%

31/07/2026 - 05:35 PM

data source: Investis Digital

Financial Results & Reports

Press releases

Financial highlights

Last trade 55.12€

Variation +2.61%

31/07/2026 - 05:35 PM

data source: Investis Digital

Financial Results & Reports

Press releases

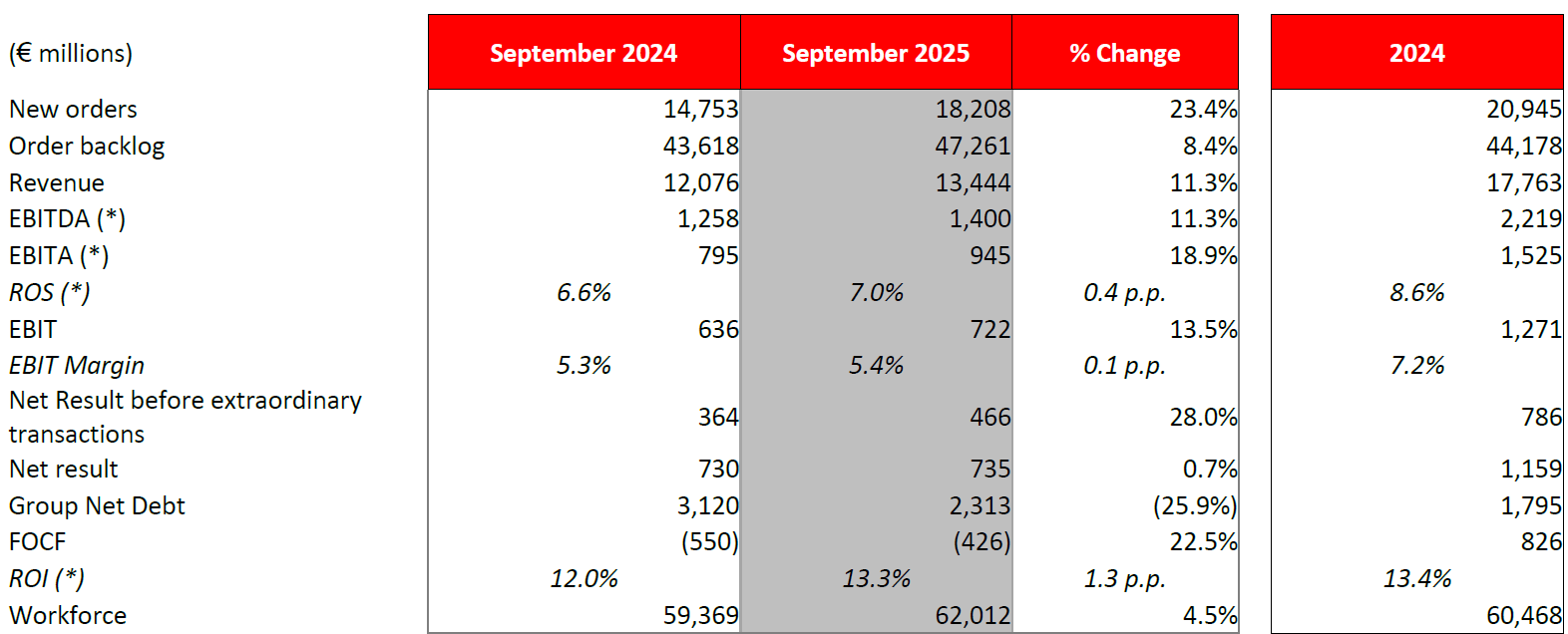

(*) Figure at 30 September 2024 is presented in restated form as a result of the revision of the KPI with reference to the valuation of strategic investments

*******************

Leonardo's Board of Directors, convened today under the Chairmanship of Stefano Pontecorvo, examined and unanimously approved the 2025 first nine months results.

“The results for the first nine months of 2025 confirm the Group’s positive performance. Steadily volume growth and solid profitability continue to underpin our competitive positioning in both domestic and international markets. We reaffirm our 2025 guidance - revised upwards last July with more ambitious targets for orders, FOCF and net debt - as well as our commitment to the timely execution of the Industrial Plan, which is progressing in line with the identified strategic priorities. We have further pursued our path of inorganic growth through the acquisition of Iveco Defence, and, in the context of strengthening European alliances, we have signed an MoU with Airbus and Thales to establish a new company in the space sector. This initiative aims to reinforce Europe’s strategic autonomy in space and further consolidates Leonardo’s role as a leading player in the Aerospace, Defence and Security domain,” stated Roberto Cingolani, Chief Executive Officer and General Manager of Leonardo. “Following the appointment of the new Chief Financial Officer, I would like to express, on behalf of the Group, our sincere gratitude to Alessandra Genco for her invaluable contribution and dedication to Leonardo over the years”, Cingolani concluded.

9M2025 financial results

The good performance of the Group was consolidated in the first nine months of 2025, confirming its competitive positioning in both domestic and international markets supported by steadily growing volumes and a solid profitability. The good performance of the period, compared with the same period of the prior year, is even more significant inasmuch as it does not include the contribution from the Underwater Armaments & Systems (UAS) business, which had been recognised under the Defence Electronics & Security sector until 2024 and sold to Fincantieri in early 2025.

In the first nine months of 2025, New Orders increased significantly reaching €bil. 18.2 (+23.4% compared to the figure of the comparative period, +24.3% compared with the like-for-like figure), confirming the continuing strengthening of the core businesses and also as a result of an important order in the Aeronautics sector, within a market environment where demand for security remains high. The book-to-bill stood at 1.4.

Revenues came to €bil. 13.4 showing a significant increase (+11.3% compared to the figure of the comparative period, +12.4% compared with the like-for-like figure), and EBITA was equal to €mil. 945 (+18.9% compared to the restated (*) figure of the comparative period, +22.7% compared with the like-for-like figure), in line with expectations and the sustainable growth path envisaged in the Industrial Plan of Leonardo.

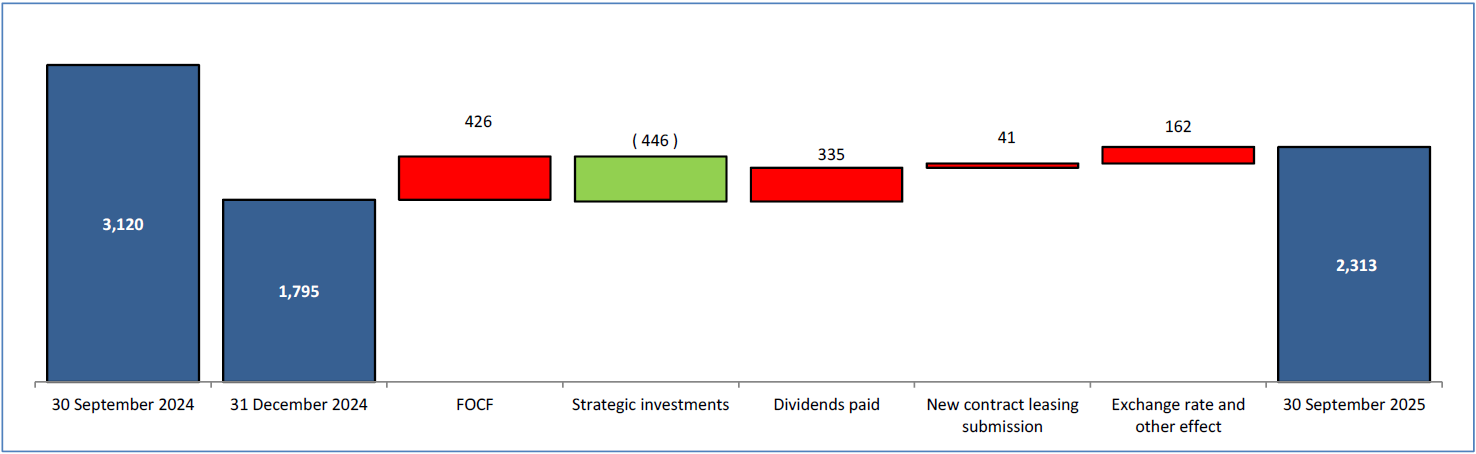

Free Operating Cash Flow, negative for €mil. 426 as a result of the usual interim trend, showed an improvement compared to the comparative period (+22.5%, +22.3% compared with the like-for-like figure) demonstrating the effectiveness of the actions undertaken. The FOCF performance and the consideration received as part of the sale of the UAS business, equal to about €mil. 446, result in a positive effect on the Group Net Debt, down by about 25.9% compared to 30 September 2024.

(*) The figure for the comparative period is presented in restated form as a result of the revision of EBITA, starting from the 2024 Financial Statements, with reference to the valuation of strategic investments.

Key Performance Indicators (KPIs)

(*) The figure at 30 September 2024 is presented in restated form as a result of the revision of the KPI with reference to the valuation of strategic investments. Specifically, starting from the 2024 Financial Statements, the share of net result of strategic investees, which is already recognised within the Group's EBITA as part of their valuation at equity, now no longer includes any non-recurring, extraordinary or non-routine items in the income statement; in line with Leonardo’s policies and the approach already applied to companies consolidated on a line-by-line basis, these items are deducted from EBITA in order to show profit margins that are not affected by volatility elements. The revision described above also impacted EBITDA and the performance indicators ROS and ROI, while it had no effects on other indicators.

As indicated above, following the finalisation of the sale to Fincantieri of the Underwater Armaments & Systems (UAS) line of business, occurred on 14 January 2025, the figures at 30 September 2025 do not include the contribution from such business that, vice versa, was recognised within the Defence Electronics & Security sector until 2024. In order to make the Group's operational performance more comparable, for some performance indicators we report below the figure of the comparative period – and the related change compared to the current period – excluding the contribution from the UAS business (like-for-like perimeter):

(*) The figure at 30 September 2024 is presented in restated form as a result of the revision of the KPI with reference to the valuation of strategic investments.

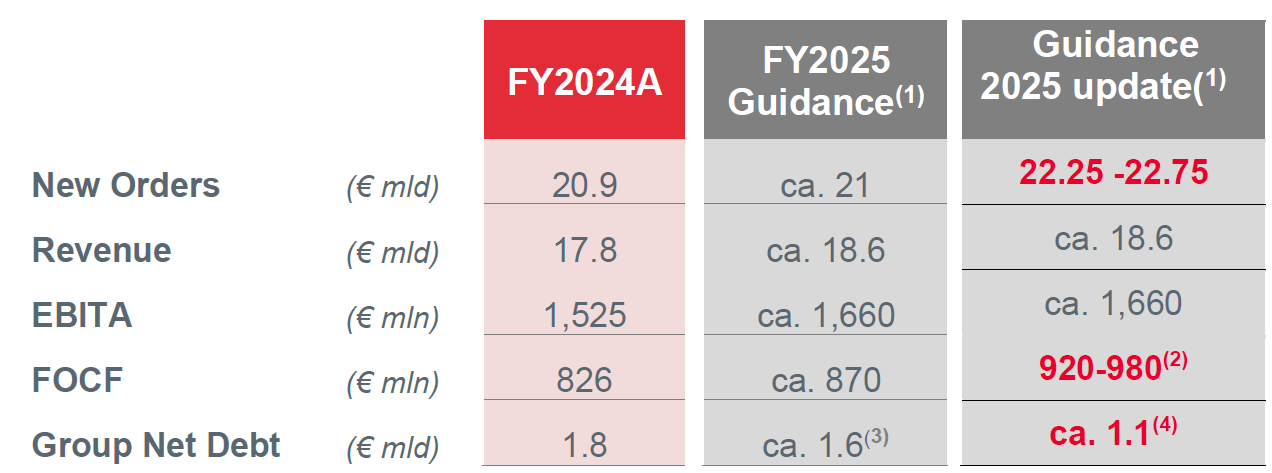

2025 Guidance

According to the first nine 2025 results and the expectations for the coming quarter, we confirm full year 2025 Guidance updated in July 2025.

This is summarised in the table below:

Based on USD/€ exchange rate at 1.08 and €/GBP exchange rate at 0.86

(1) Based on the current assessments of the impacts of the geopolitical situation also on supply chain, tariffs, inflationary levels and the global economy, subject to any further significant effects

(2) Including the effects deriving from the resolution of the dispute concerning the Norwegian NH90-program

(3) Assuming the increased dividend payments from €0.28 to €0.52 per share, M&A transaction of ca. €500 million, DRS shareholders remuneration, new leasing contracts and other minor movements

(4) Assuming the increased dividend payments from €0.28 to €0.52 per share, M&A transaction of ca. €100 million, DRS shareholders remuneration, new leasing contracts and other minor movements

Commercial performance

Business performance

Financial performance

The Group Net Debt, equal to €mil. 2,313, decreased compared to September 2024 (down about €bil. 0.8), thanks to the strengthening of the Group's cash generation and to the cash-in of the total amount of €mil. 446 arising from the sale of the UAS business.

Compared to 31 December 2024 (€mil. 1,795) the figure increased mainly as a result of the abovementioned FOCF performance, net of the effect of the abovementioned sale of the UAS business, in addition to the dividends paid for an amount of €mil. 335 (of which €mil. 298 related to Leonardo S.p.a. that, in line with that communicated on the occasion of the 2025-2029 Industrial Plan, paid a dividend almost doubled equal to € 0.52 per share in 2025 vs € 0.28 per share in 2024).

Changes in the Group Net Debt

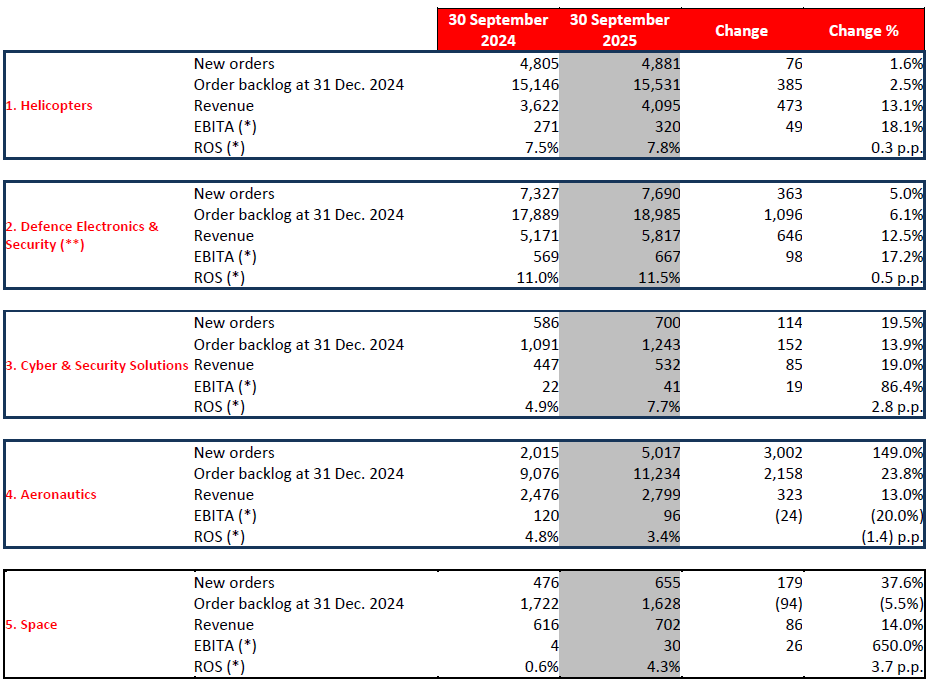

Key performance indicators by Sector

Leonardo confirms its growth path in all core Sectors of its business. The business sectors are commented on below in terms of business and financial performance:

(*) 2024 restated figure as a result of the revision of the KPI with reference to the valuation of strategic investments.

(**) 2024 figure not including the contribution from the Underwater Armaments & Systems (UAS) business (isoperimeter).