12 March 2024 08:30 Inside Information

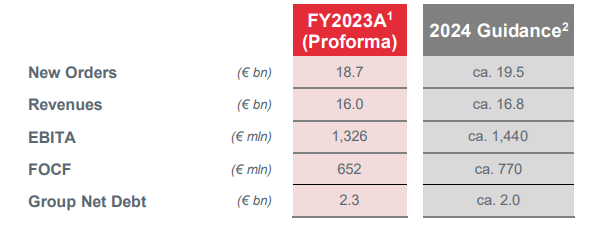

2024 GUIDANCE

Based on the current assessment of the effects deriving from the geopolitical situation on the supply chain and the global economy and assuming no additional major deterioration

- Order of ca. € 19.5 billion

- Revenues of € 16.8 billion

- EBITA € 1,440 million

- Free Operating Cash Flow of ca. € 770 million

- Group Net Debt of ca. € 2.0 billion

RESULTS

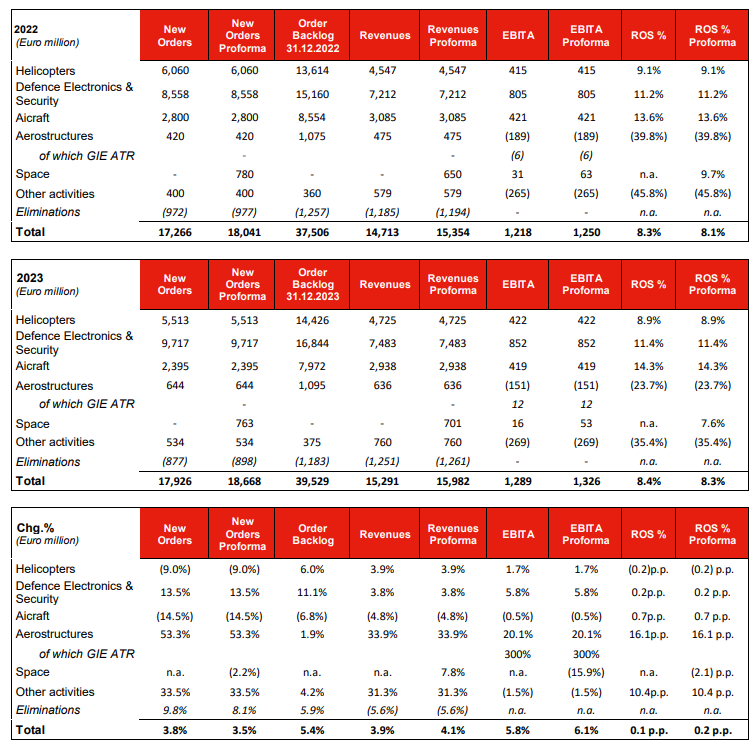

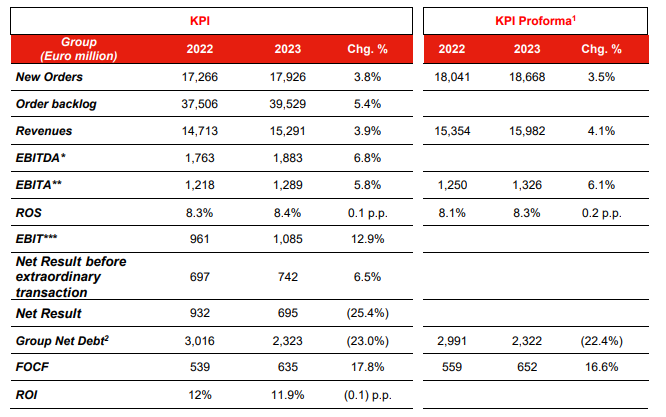

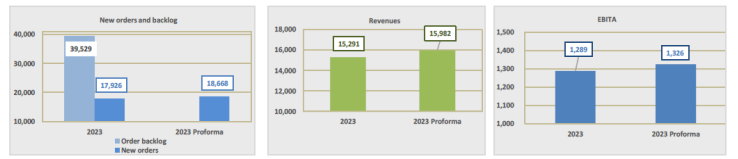

- Orders of € 17.9 billion (+3.8% vs 2022), with a book-to-bill of 1.2x

- Revenues of € 15.3 billion (+3.9% vs 2022), reflecting growth across all Divisions

- EBITA of € 1.29 billion (+5.8% vs 2022)

- Net Result before extraordinary transaction of € 742 million (+6.5% vs 2022), mainly reflecting EBIT performance

- Net Results of € 695 million, -25,4% vs 2022, whose figure reflected the capital gain obtained from the sales of Leonardo DRS Global Enterprise Solutions and Advanced Acoustic Concepts businesses

- Free Operating Cash Flow of € 635 million (17.8% vs 2022), driven by topline growth and cost & investment discipline

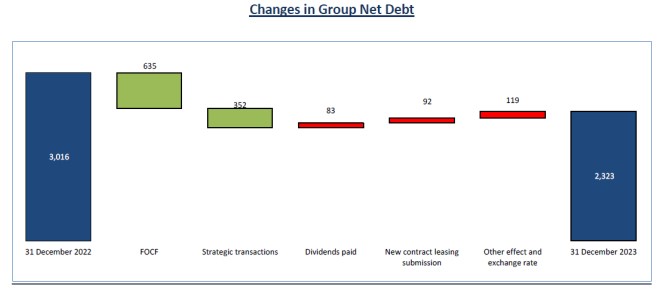

- Group Net Debt, of € 2,323 million, -23% versus € 3,016 million in 2022

Leonardo's Board of Directors, convened today under the Chairmanship of Stefano Pontecorvo, examined and unanimously approved the full year 2023 results.

FY 2023 Results

The financial results for 2023 confirm the performance of the Group, with a particularly positive trend in cash-flow generation in the period.

As described in more detail below, pro-forma KPIs are provided in addition to the ordinary KPIs to reflect the upcoming consolidation of the Telespazio group.

New orders showed steady, structural growth, nearing the threshold of €bil. 18 (€bil. 18.7 of the pro-forma figure), with a particularly positive performance in the European component of the Defence Electronics & Security business. The sustainability of commercial growth is even more pronounced considering that New orders in 2022 included the order from the Polish Ministry of Defence for the AW149 helicopters.

Revenues showed an increase of 3.9% (4.1% compared to the pro-forma figure), thanks also to the remarkable recovery of the Aerostructures (+34%) and the performance of Defence Electronics & Security and of Helicopters. The growth of revenues is accompanied by an increase in EBITA of 5.8% (6.1% compared to the pro-forma figure).

The EBITA continued to be driven by Defence Electronics & Security, with a particular contribution from the European component, and by the recovery of Aerostructures, bringing ROS to 8.4 %.

Remarkable financial performance, with the free operating cash flows (FOCF) showing an increase of 18% compared with the figure recorded in 2022, which demonstrates the Group’s ability to keep on the path to strengthen cash generation it has embarked on.

The Group net debt continued to decrease, with an improvement of 23% from 2022, standing at €bil. 2.3; the significant cash-flow generation and the proceeds from the sale of the minority stake in DRS allowed the Group to continue the process of reducing its indebtedness.

Key Performance Indicator and comparison with and without Telespazio consolidation

Pro-forma data are also provided in relation to some Key Performance Indicators which translate in numbers the notional effect of the line-by-line consolidation of Telespazio. The aim is to already provide an indicator which is representative of the KPIs that will be presented from 2024:

Key Performance Indicator and comparison with and without Telespazio consolidation

Pro-forma data are also provided in relation to some Key Performance Indicators which translate in

numbers the notional effect of the line-by-line consolidation of Telespazio. The aim is to already provide

an indicator which is representative of the KPIs that will be presented from 2024:

1 Telespazio fully consolidated

2 Net Debt include the effect deriving from DRS transaction

(*) EBITDA is given by EBITA, as defined below, before amortisation and depreciation (excluding amortisation of intangible assets arising from business combinations) and impairment losses (net of those relating to goodwill or classified among “non-recurring costs”).

(**) EBITA is obtained by eliminating from EBIT the following items: any impairment in goodwill; amortisation and impairment, if any, of the portion of the purchase price allocated to intangible assets as part of business combinations, restructuring costs that are a part of defined and significant plans; other exceptional costs or income, i.e. connected to particularly significant events that are not related to the ordinary performance of the business.

(***) EBIT is obtained by adding to Income before tax and financial expenses (defined as earnings before “financial income and expense”, “share of profits (losses) of equity- accounted investees”, “income taxes” and “Profit (loss) from discontinued operations”) the Group’s share of profit in the results of its strategic investments (MBDA, GIE ATR, TAS, Telespazio and Hensoldt), reported in the “share of profits (losses) of equity-accounted investees”.

2024 GUIDANCE

The expected 2024 performance confirms the sustainable growth path accompanied by increasing profitability and cash flow generation, in a context characterized by high demand for defense and security.

The actions that have been promptly implemented by the Group allow the mitigation of effects generated by inflationary pressures due to the Russia-Ukraine conflict.

Based on the current assessment of the effects deriving from the geopolitical situation on supply chain, inflation and global economy, and assuming no additional major deterioration, Leonardo expects to deliver in 2024:

- Progressive growth in new orders of ca. € 19.5 billion, driven mainly by Defence Electronics & Security and by the continuing recovery of the Aeronautics sector, confirming a strong positioning of the Group's products and solutions and presence in key markets

- Revenues of € 16.8 billion, up compared to 2023, thanks to the contribution of new orders and the development of portfolio activities, delivering off a backlog at a record value of ca. € 40 billion

- Increasing profitability, with EBITA of € 1,440 million, driven by growth in volumes and confirmed solid industrial profitability of the main business areas. The estimated improvement in profit also reflects the progressive recovery of the Aerostructures business, and is notwithstanding the difficulties in the manufacturing segment of satellites for commercial telecommunications through its subsidiary TAS

- FOCF of ca. € 770 million, with the defence/governmental business delivering solid cash generation, while Aerostructures continues to absorb slightly less cash than 2023

- Group Net Debt of ca. € 2.0 billion driven by cash flow generation and assuming the increased dividend payment from € 0.14 to € 0.28 per share, new leasing contracts, strategic investments, and other minor transactions

Below is the summary table:

Exchange rate assumptions: €/USD= 1.15 and €/GBP= 0.89

1 The values shown for the year 2023 enhance the full consolidation of Telespazio which will be operational from 2024

2 Based on the current assessment of the effects deriving from the geopolitical situation on the supply chain and the global economy and assuming no additional major deterioration

Commercial Performance

- New Orders, amounted to EUR 17,926 million (€bil. 18.7 of the pro-forma figure), showing a growth from 2022 (+3.8%, +3.5% compared to pro-forma data), thanks to the major contribution given by Defence Electronics & Security, in all business areas of its European component. The increase in the year represents an important sign of consolidation for the Group considering that the comparative figure included the important acquisition of the order for AW149 helicopters from the Polish Ministry of Defense (€bil. 1.4).

The trend in New orders clearly highlights the effectiveness of the Leonardo Group's commercial offer thanks to a diversified offering, widespread geographic distribution of its sales organization and the competitiveness of the Group. Quality of products and integrated solutions that meet the complex operational requirements imposed by the customers, and innovation are the Group's sound distinguishing features that have made it possible to strengthen and expand the Group's market presence, which, despite the lack of major individual orders, allow for the growth of the portfolio of future businesses.

The aforesaid level of new orders corresponds to a book-to-bill (ratio of New Orders to Revenues for the period) equal to about 1.2

- Backlog, amounted to EUR 39,529 million ensures a coverage in terms of equivalent production equal to 2.6 years (2.5 years in 2022), nearing the threshold of €bil. 40 thanks to the success of the commercial campaigns begun in the last years

Economic Performance

- Revenues, amounted to EUR 15,291 million (€bil. 16 of the pro-forma figure), were increasing compared to 2022 (+3.9%, +4.1% against pro-forma data) in almost all business areas, including Aerostructures, which benefitted from the resumption of deliveries of B-787. Particularly significant is the contribution from the European component of Defence Electronics & Security.

- EBITA, amounted to EUR 1,289 million, (€mil. 1,326 of the pro-forma figure) reflects the solid performance of the Group businesses and showed a growth on 2022 (+5.8%, +6.1% compared to pro-forma data) thanks to the major contribution from the European component of Defence Electronics & Security and the lower loss in Aerostructures, in line with the plan to revive the business and thereby confirming the gradual recovery in civil aeronautics.

- EBIT, amounted to EUR 1,085 million benefitted, compared to 2022 (€mil. 961), from the improvement of EBITA, as well as from the lower incidence of the restructuring costs due to the ongoing early retirement plans.

- The Net result before extraordinary transactions, amounted to EUR 742 million (€mil. 697 in 2022), reflects the performance of EBIT, and the taxation that in 2022 mainly benefitted from a lower tax burden on foreign companies.

- The Net Result, amounted to EUR 695 million (€mil. 932 in 2022) included, in addition to the Net result before extraordinary transactions, the recognition for €mil. 57 of costs for the evaluation of the road transport business in view of future disposal, net of a capital gain of €mil. 10 relating to the disposal of the ATM business unit by Selex ES Llc set out in the “Industrial Transactions” section. The 2022 figure, on the contrary, reflected the capital gain obtained from the sales of Leonardo DRS Global Enterprise Solutions and Advanced Acoustic Concepts businesses.

Financial Performance

- Free Operating Cash Flow (FOCF), positive for EUR 635 million (€mil. 652 of the pro-forma figure), showed an increase of 17.8% compared to the 2022 FOCF of €mil. 539 (+16.6% on the pro-forma figure €mil. 559), confirming the positive trend that had already been highlighted in recent years. The targets achieved are due to the actions aimed at strengthening the performance of operations, a careful investment policy in a period of business growth, to the streamlining and making working capital more efficient and to an effective financial strategy.

- Group Net Debt, of EUR 2,323 million showed an improvement compared to 31 December 2022 (€mil. 3,016); the figure benefitted from the aforesaid trend in the FOCF while also including the financial effects of the transactions that are described below

- the sale completed in November of Leonardo DRS ordinary shares (a transaction widely described in section “Industrial and financial transactions”), which resulted in a cash-in – after transaction costs – of about €mil. 327 (USDmil. 352);

- the sale, completed in May by the US subsidiary Selex ES Llc, of the business unit of Air Traffic Management (“ATM”) to Indra Air Traffic, Inc., fully owned by the Spanish company Indra Sistemas S.A., for a total amount of about USDmil. 37;

- the dividend that was paid in July for €mil. 83;

- the execution of new lease agreements for €mil. 92;

- translation of foreign currency positions and other items

As at 31 December 2023, Leonardo S.p.A. had sources of liquidity available for a total of about €mil. 4,210 to meet the financing needs of the Group’s recurring operations, broken down as follows:

- an ESG-linked Revolving Credit Facility for an amount of €mil. 2,400, divided into two tranches of €mil. 600 and €mil. 1,800 expiring on 7 October 2024 and 7 October 2026 respectively;

- additional unconfirmed short-term lines of credit of about €mil. 810;

- a framework programme for the issue of commercial papers on the European market (Multi- Currency Commercial Paper Programme) for a maximum amount of €bil. 1 expiring on 2 August 2025.

The Company also has a €mil. 260 Sustainability-linked financing granted by the European Investment Bank (EIB) – with a contract signed in November 2022 – entirely unused at the date of this report.

Furthermore, Leonardo has unconfirmed lines of credit for a total of €mil. 10,877, of which €mil. 3,051, still available as at 31 December 2023.

Finally, other Group subsidiaries have the following credit facilities:

- Leonardo DRS has a Revolving Credit Facility for an amount of USDmil. 275 (€mil. 249), which was entered into at the same time as the completion of the merger with RADA, entirely unused at 31 December 2023;

- Leonardo US Corporation has short-term revocable credit lines, guaranteed by Leonardo Spa, for USDmil. 210 (€mil. 190), which had been used for USDmil. 40 at 31 December 2023 (€mil. 36);

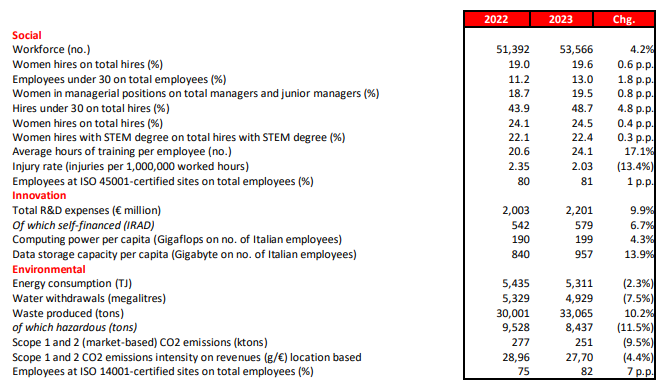

ESG PERFORMANCE INDICATORS

SECTOR PERFORMANCE

Leonardo continued the path to growth in all sectors of its core business. As pointed out above, in this Annual Financial Report a set of Key Performance Indicators are provided for to represent the business performance considering the entire contribution from Telespazio group, in consideration of its upcoming consolidation in 2024.